The global private equity (PE) industry in 2026 is currently navigating one of the most severe liquidity bottlenecks in its entire history. For decades, the traditional machinery of private equity operated on a predictable, highly lucrative rhythm: buy an underperforming asset, improve its operations over a three to five-year window, sell it for a substantial premium, and distribute the resulting profits—known as carried interest—to executives and investors. Today, that machinery has fundamentally stalled.

Caught in an ongoing drought of initial public offerings (IPOs) and mergers and acquisitions (M&A), the industry is grappling with a massive backlog of aging assets. With trillions of dollars trapped in unrealized value, fund managers have turned to aggressive financial engineering to manufacture liquidity. The explosive rise of carried interest loans and Net Asset Value (NAV) lending has introduced a new layer of systemic leverage to the private markets. As hold periods lengthen and valuation markdowns loom, the industry faces a brewing storm of potential defaults.

The Mechanics of Carried Interest and the “Exit Overhang”

To understand the current crisis, one must first understand how private equity compensation diverges from other alternative assets. If you run a hedge fund and your portfolio appreciates by $1 billion in a given year, you can immediately charge performance fees on that mark-to-market return. Conventionally, these fees sit at 20% of returns, yielding a $200 million payout that can be used to pay traders, fund lifestyles, or buy luxury assets.

If you run a private equity fund, the mechanics are vastly different. Private equity firms do not generally charge performance fees on mark-to-market returns, primarily because there is no liquid public market to mark those assets to. If a firm executes a leveraged buyout of a company for $5 billion, and internal models suggest it is worth $6 billion the following year, that valuation remains highly subjective and inherently conflicted. Instead, performance fees—carried interest—are only collected upon the actual sale of the company. In that scenario, selling the $5 billion acquisition for $6 billion generates $1 billion in realized gains, unlocking the $200 million in carry all at once.

In a hypothetical steady state, a large private equity business is constantly buying new companies and selling older ones, creating a smooth, annual pipeline of carried interest realizations. But 2026 is far from a steady state. When realizations dry up, fund managers collect very little actual cash, regardless of how strong their paper returns appear to be.

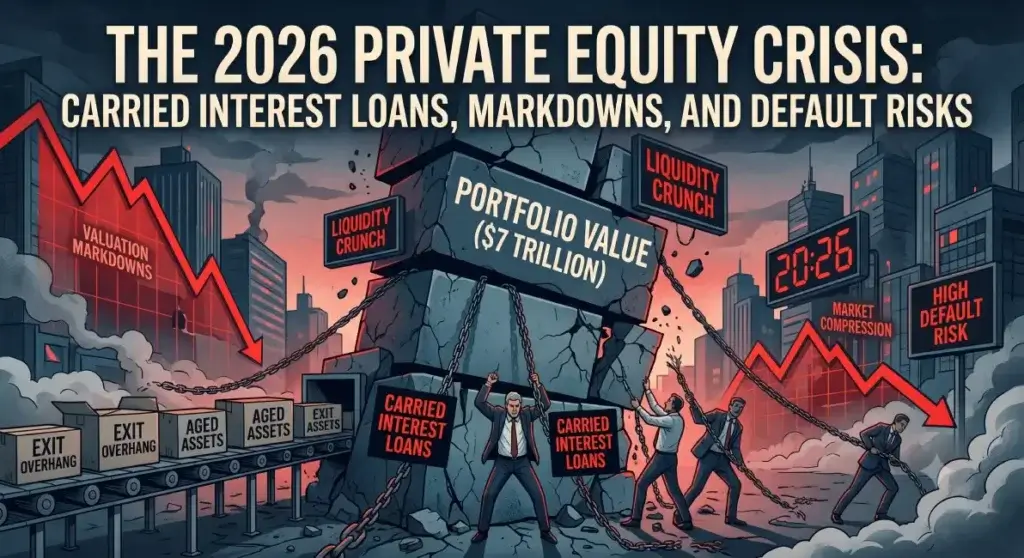

This dynamic has created what industry insiders call the “exit overhang”. The data from late 2025 and early 2026 paints a stark and troubling picture of deteriorating profits and delayed timelines. Currently, there are over 32,900 unsold companies sitting in global private equity portfolios. This massive backlog represents a staggering $5 trillion in unrealized, trapped value—a figure that pushes closer to $7 trillion when factoring in growth equity investments.

Because of the frozen exit environment, hold periods have stretched significantly. According to Bain & Company, average hold periods are now seven years, up from the historical norm of five to six years. Consequently, the industry’s inventory-to-exit ratio has spiked to roughly 10.9x, far above the historical average of 6.9x. Today, approximately 16% of all PE-owned companies are 8 to 12 years old, which is a significant increase from the historical norm of 13%.

Valuation Compression: The Fading Mirage of Returns

Compounding the problem of aging portfolios is the harsh reality of valuation compression. Funds that aggressively purchased assets at peak valuations during the 2021–2022 frenzy are now facing severe margin deterioration. The macroeconomic environment has shifted; higher interest rates and the rising cost of private credit have systematically eaten into the free cash flow of portfolio companies.

The critical metric known as the “exit spread”—the multiple expansion achieved from the entry of a deal to its eventual exit—has compressed violently, dropping from a historical average of 4 points down to a mere 1.6 points. Managers who confidently expected to sell their assets at a premium are now forced to hold them indefinitely. As these hold periods drag on, projected Internal Rates of Return (IRRs) evaporate, taking expected carried interest down with them.

Furthermore, the structure and taxation of carry are under unprecedented pressure. To retain frustrated executives who are searching elsewhere for more predictable compensation, firms are actively renegotiating carry structures. Many are shifting away from traditional “whole-fund” European waterfalls toward more immediate “deal-by-deal” carry structures with shorter vesting periods. Simultaneously, regulatory pressures are mounting globally. In the UK, for example, carried interest was officially reclassified as income starting in April 2026. This regulatory shift raised the effective tax rate on these profits from the previous 28% capital gains rate to roughly 34.1%, heavily compressing the net take-home pay of European dealmakers.

The Financial Engineering Boom: Manufacturing Liquidity

Faced with a devastating M&A drought, delayed payouts, and the need for cash, the industry has turned to financial engineering. What managers want is a financial product that smooths their lumpy, delayed carried interest into something resembling a steady, mark-to-market performance fee.

This demand has birthed an explosive market for leverage at two distinct levels: institutional Net Asset Value (NAV) loans for the funds themselves, and personal carried interest loans for the executives.

Institutional NAV Lending

At the fund level, General Partners (GPs) are heavily utilizing NAV loans. Rather than borrowing against individual assets, these loans are collateralized by the combined paper value of a fund’s entire underlying portfolio. GPs are using this borrowed cash to artificially distribute capital back to their Limited Partners (LPs). This manufactured liquidity helps secure LP commitments for future fundraising cycles, or it is used defensively to inject vital capital into struggling, cash-starved portfolio companies.

The scale of NAV lending is staggering. The total outstanding exposure of the NAV loan market currently sits at roughly $150 billion. Driven by an explosive 30% annual growth rate over the last five years, this market is projected to reach $350 billion by 2030. According to recent data from Hamilton Lane, 10% of all GPs globally currently hold an active NAV loan, while another 11% are actively seeking one.

While major global investment banks traditionally dominated this space, specialized private credit firms have aggressively stepped in to meet the 2025 and 2026 demand. Key players now include 17Capital, recognized as the undisputed heavyweight in pure-play NAV lending, which recently closed a massive $7.5 billion credit fund to feed this demand. Other major players include Pemberton Asset Management, which launched a $1 billion+ NAV-financing fund backed by the Abu Dhabi Investment Authority, alongside Apollo Global Management and Ares Management, both of which have rapidly expanded their fund-finance arms. In total, specialized lenders raised a record $12.9 billion for NAV strategies in 2025 alone.

Executive-Level Carried Interest Loans

At the executive level, exposure is growing just as fast. Because the exit drought has starved dealmakers of actual cash payouts, they are increasingly taking out personal loans collateralized by their forecasted future share of profits to maintain their lifestyles, fund required co-investments into newer funds, or buy properties.

These are highly bespoke loans underwritten by the elite private wealth divisions of major banks, as traditional collateral like real estate or liquid stock is often missing. Major institutions actively offering these loans include:

Citi (Citi Global Wealth at Work): Offers a structured “Partner Capital Loan Program” tailored for alternative asset managers.

UBS and Deutsche Bank: Operate heavily in this space for high-net-worth dealmakers in the U.S. and Europe.

JPMorgan Chase: Handles these requests through its Private Bank U.S. Lending Services division, structuring them as complex securities-based lines of credit linked to fund performance.

CIBC Commercial Banking: Provides specific “Partner Capital and Shareholder Loans” for executives needing to fund equity requirements.

The surge in demand has also created a massive boom for specialist brokers like London-based Enness Global, which structures these deals and secures upwards of 50% Loan-to-Value (LTV) on pure forecast carry. Enness Global’s CEO, Islay Robinson, noted that the firm had been closing two to three transactions per month—significantly more than in previous years. Recently, the broker reported a massive spike of 459 high-net-worth inquiries for carried interest loans in just a six-month window, more than tripling the 134 inquiries seen during the exact same period the prior year. Remarkably, some of these loans are secured against the carry alone, meaning the lender cannot seize the executive’s personal assets if the forecast profit share never actually materializes.

The Ticking Debt Bomb: Default Risks and the “Marks” Dilemma

While historical default rates in fund finance have been virtually nonexistent, the landscape in 2026 is testing the structural limits of these loans due to broader macroeconomic stress. The foundational risk underpinning this $150+ billion in exposure is directly tied to the “marks”—the GPs’ self-reported valuations of their underlying companies.

Currently, lenders consider this exposure “safe” because they issue these loans with massive LTV cushions, typically lending only 5% to 30% of a fund’s total reported portfolio value. However, the collateral underpinning this debt is the roughly $5 trillion in unrealized value across 32,900 unsold companies. If macroeconomic conditions force private equity firms to finally mark down this mountain of aging assets to their true, compressed market value, that LTV cushion will evaporate instantly.

An aggressive market correction that spikes LTV ratios could breach debt covenants. This would trigger mandatory cash sweeps or, catastrophically, allow lenders to force the sale of the fund’s underlying assets at fire-sale prices.

The fundamental risk driving this scenario is the deteriorating health of the underlying companies. Roughly 40% of private-credit borrowers are currently carrying negative free cash flow. Compounding this stress is a massive wall of debt maturing between 2026 and 2028. UBS has warned that in an aggressive disruption scenario, underlying US private credit default rates could climb as high as 15%.

If these companies fail, or if a fund simply fails to clear its hurdle rate upon ultimate exit, the carried interest pool goes to absolute zero. Executives who took out standard bank loans or personal “deemed loans” against their forecast carry will suddenly find themselves deeply underwater, lacking the expected cash windfall required to pay off the principal. This places both institutional NAV loans and executives’ personal carry loans at an acute, heightened risk of restructuring or outright default.

Actionable Insights for 2026 and Beyond

The current environment demands strategic recalibration from all stakeholders in the private equity ecosystem.

For Limited Partners (LPs): Scrutinize the use of NAV loans within your portfolio. Distributions funded by NAV loans are essentially returning capital using borrowed money against assets you already own. LPs must aggressively evaluate the true market value of the GPs’ “marks” and demand transparency on how debt is being utilized at the fund level.

For General Partners (GPs): Prepare for forced markdowns. The $5 to $7 trillion exit overhang cannot be sustained indefinitely. GPs should stress-test their portfolios against the UBS 15% default rate scenario and proactively negotiate covenant flexibility with their NAV lenders before LTV thresholds are breached.

For Dealmakers and Executives: Exercise extreme caution with personal carried interest loans. With hold periods stretching to seven years and exit spreads compressing to 1.6 points, the forecasted carry of 2021 is unlikely to materialize. Ensure that personal borrowing is structured on a non-recourse basis wherever possible to protect personal assets if fund hurdle rates are not met.

Embrace Restructuring: GPs must be willing to shift away from traditional whole-fund European waterfalls to deal-by-deal structures. Offering shorter vesting periods will be critical to retaining top talent who are starved of liquidity and facing higher tax burdens, particularly in jurisdictions like the UK.

What to Expect on the Horizon

Ultimately, the entire private equity industry is currently engaged in a high-stakes waiting game. The sector is betting heavily that a broadly accommodating macroeconomic environment in late 2026 and 2027 will allow them to eventually sell their historic backlog at current paper valuations. However, if that bet fails, the illusions of paper wealth will shatter. Should forced markdowns become reality, both the multi-billion-dollar NAV loans sustaining the funds and the bespoke personal loans sustaining the executives will be pushed to the brink of default, forever altering the landscape of alternative investments moving forward.