Relying on traditional macroeconomic data to drive portfolio strategy is a lot like driving a racecar while staring into the rearview mirror. By the time lagging indicators like CPI or retail sales are published, the market has already moved. To capture consistent alpha, investors must identify real-time structural shifts—specifically, the mechanics of retail leverage. This is precisely how the Retail Investor Margin Propensity Index (RIMPI), developed by our subsidiary Polar Works, gave forward-looking traders the framework to anticipate the massive H1 2022 market downturn and meme-stock collapse.

Measuring the Fuel of Market Froth

Unlike traditional metrics that look at total margin debt balances after the fact, RIMPI aggregates real-time behavioral data to measure the immediate likelihood of retail investors increasing their margin debt. It answers a foundational question: Is the retail crowd aggressively buying on leverage right now, or are they pulling back?

When RIMPI flashes an “Extreme” score, it indicates euphoric risk-taking. At this peak, there is no marginal buyer left to push equities higher, leaving the entire financial system fragile and highly vulnerable to sudden liquidity shocks.

The December 2, 2021 Signal

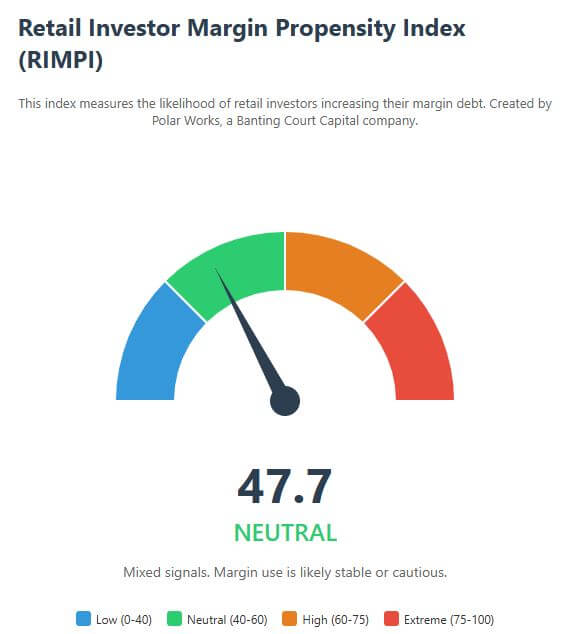

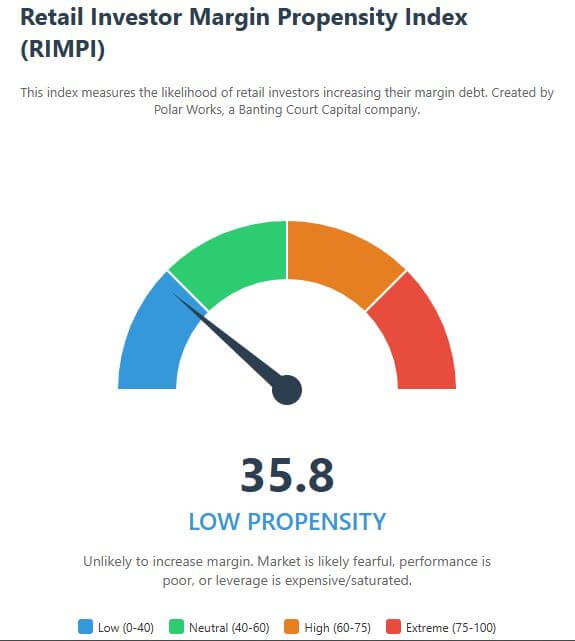

According to the photo above, the index registered a Neutral score of 47.7 on December 2, 2021. At that precise moment, the gauge indicated “mixed signals” where margin use was “stable or cautious.” Although the score is technically neutral, it’s only 7.7 points aware from registering “low” which would nearly guarantee retail deleveraging. However, by January 20th, 2022 the index score had fallen to 35.8 which officially registers as “low”, by this time the S&P 500 closed at 4,482 which was down 6.5% from its high of approximately 4,792. From that point the S&P 500 continued to capitulate until it went below 3,700 in June.

However, the true value of RIMPI lies in its ability to act as a leading indicator of momentum inflections. As noted by Polar Works, a historical back test of this framework successfully predicted the infamous 2022 meme-stock collapse a full four weeks early. By diagnosing the rapid accumulation and eventual exhaustion of retail leverage before it hit mainstream headlines, the index flagged the exact moment the speculative floor was about to give way.