To the average retail investor, the stock market is a simple machine. Price is driven by supply and demand, reflected clearly on a public exchange order book or a candlestick chart. You watch the futures market to gauge sentiment, analyze volume bars to confirm a breakout, and assume that every participant is playing by the same structural rules.

It is a comforting perspective. It is also entirely wrong.

Beneath the visible surface of public tickers and exchange-traded contracts lies an elite, opaque layer of the financial system: the over-the-counter (OTC) derivative structuring market. While regulations have evolved and historical loopholes like Prepaid Variable Forward Contracts (PVFCs) have been stripped from the modern post-IPO playbook, Wall Street’s engineering desks have simply evolved. Today, multi-billion-dollar hedge funds and investment banks do not buy or sell assets to express a basic market view. Instead, they engineer highly complex financial instruments designed to extract specific profit profiles, shift risk, and control market direction—all while leaving zero initial footprint on the public exchanges retail traders use to make decisions.

Whether it is a macro fund masking massive positioning without touching the futures market, or an algorithmic desk weaponizing intraday liquidity to pin a stock’s price, institutional players operate with a massive structural advantage.

To survive as a modern trader, you have to look past the charts and understand the underlying mechanics of modern derivative structuring, how it alters spot market prices, and how you can track the invisible footprints left behind by Wall Street’s engineering desks.

The Top 5 Sneaky Derivative Structures Controlling the Market

Modern institutional trading is no longer about picking winning stocks; it is about exploiting structural plumbing. Here are the top five derivative frameworks engineered by institutions that quietly dictate price action under the noses of retail investors.

1. Total Return Swaps (TRS): The Hidden Leverage Engine

When a hedge fund wants to accumulate a massive multi-billion-dollar position in a major public equity without tipping off the market or triggering regulatory disclosure requirements, they bypass the public exchanges entirely. They walk up to the equity derivatives desk of a prime broker and request a Total Return Swap (TRS).

In a TRS, the hedge fund agrees to pay the investment bank a fixed or floating interest rate in exchange for the total financial performance of an underlying asset—including capital gains and dividends.

The asymmetry here is profound. The hedge fund does not legally own a single share or futures contract; the investment bank buys the physical underlying asset to hedge their side of the swap. Consequently, the hedge fund’s name never appears on standard regulatory filings. This allows institutions to quietly build massive, highly leveraged dominant positions, completely distorting the true available float of a stock while retail traders are left analyzing standard, incomplete volume bars.

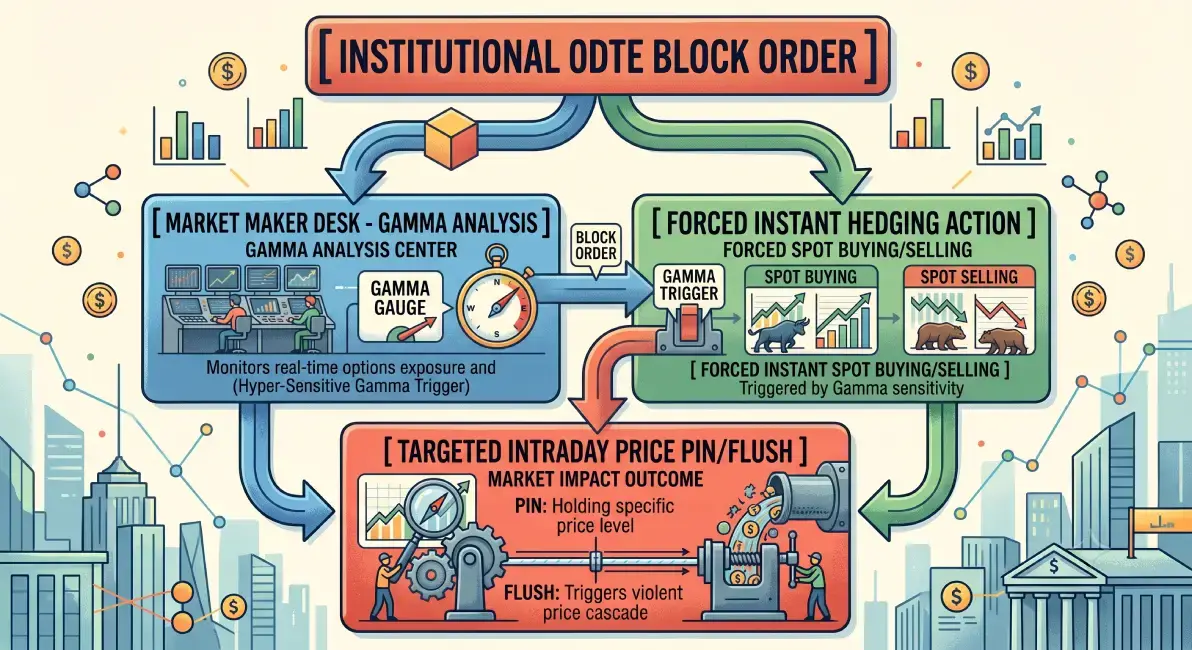

2. Zero Day to Expiration Options (0DTE): The Intraday Algorithmic Weapon

The explosion of 0DTE options is frequently framed as a retail gambling phenomenon. In reality, institutional quantitative desks utilize 0DTE flows as a highly sophisticated tool to weaponize dealer delta hedging and systematically dictate intraday price targets.

Because 0DTE options decay to zero within hours, their Gamma (the rate of change of Delta) is hyper-sensitive. When an institution floods the tape with a massive block of 0DTE calls or puts, market-making desks are forced to instantly buy or sell millions of shares of the underlying index or stock to maintain a delta-neutral book.

By calculatedly injecting 0DTE flow at critical technical inflection points, institutions can trigger self-fulfilling gamma squeezes or cascading flushes, effectively forcing market maker algorithms to run retail stop-losses for them.

3. Dividend Swaps: Stripping and Trading Pure Cash Streams

A dividend swap allows an institution to completely isolate and trade a company’s future dividend payments independently of its actual stock price. One party pays a structured fixed rate, while the other pays the actual floating dividends declared by the underlying corporation over a specific period.

While this sounds like a corporate accounting tool, macro hedge funds use dividend swaps to execute massive arbitrage plays against the spot and futures markets. Because the pricing of equity futures and standard options contracts is mathematically tethered to expected dividends, institutional distortion of the dividend swap market causes immediate, artificial adjustments to spot-futures parity.

Retail traders watching a stock head into an ex-dividend date often experience sudden, inexplicable selling pressure or violent option mispricings, entirely unaware that a multi-strategy fund is aggressively rebalancing a massive dividend swap hedge under the hood.

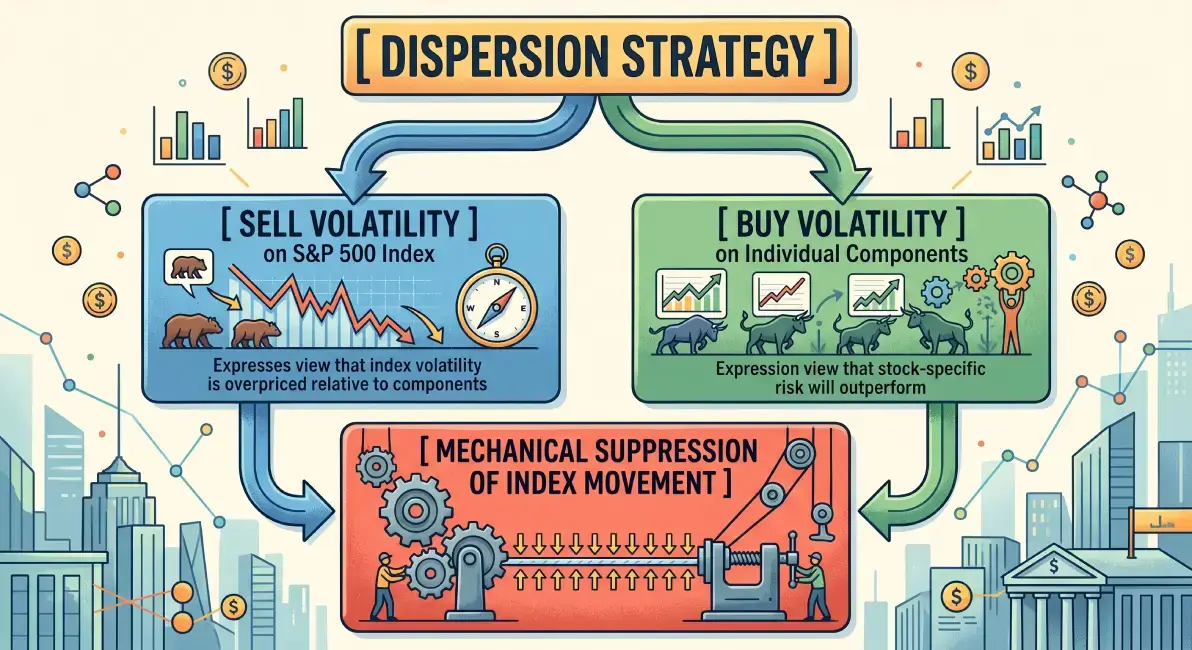

4. Custom Volatility Swaps and “Dispersion” Trades

A volatility swap is a forward contract with a payoff based purely on the realized volatility of an underlying asset, completely independent of price direction. When deployed at scale across an entire index, this evolves into the highly lucrative institutional playground known as the Dispersion Trade.

In a classic dispersion trade, a hedge fund sells volatility options on a major index (like the S&P 500) while simultaneously buying volatility options on the individual component stocks within that index.

This structural trade creates a powerful, mechanical dampening effect on the broader market. The constant institutional selling of index volatility forces market makers to continuously hedge in a way that dampens index-level breakouts. The result? The index appears completely range-bound and dead, while individual stocks under the hood experience erratic, highly volatile churn (sound familiar? Q3 2026?). Retail index traders get chopped to pieces by the artificial suppression, while the dispersion desks harvest pure structural premium.

5. Structured Notes with Hidden Barrier Options

Investment banks frequently market “structured notes” or “yield-enhancement products” to affluent retail clients and private wealth networks, promising steady yield with downside protection. What they rarely explain is that these notes are built by embedding a sneaky derivative known as a Hidden Barrier Option.

The note might promise a 10% coupon as long as a underlying stock doesn’t drop past a specific “knock-in barrier” (e.g., 30% below current prices). If the stock hits that barrier, the protection vanishes, and the retail investor takes the full brunt of the loss.

The institutional trap lies in the bank’s mandatory hedging behavior. As the underlying stock declines and creeps closer to that critical 30% barrier level, the issuing bank’s trading desk is structurally forced to short-sell exponentially more shares of the stock to hedge their mounting structural liability. This creates a terrifying, self-fulfilling downward spiral that magnetically pulls the stock straight through the retail barrier, knocking out the investor’s protection and locking in institutional profits.

The Retail Playbook: Exploiting the Options and Futures Market

You cannot beat institutional desks at the structuring game. They have the capital, the legal teams, and direct access to internal liquidity pools. However, you do not have to play their game blindfolded. Every custom derivative structured by a bank or a hedge fund eventually forces an underlying transaction in the public spot, options, or futures market to hedge the risk.

By understanding where these giant structural waves are forming, you can position your options and futures trades to ride the coattails of forced institutional flow.

1. Map Out Dealer Gamma and Delta Exposure (GEX/DEX)

Because market makers are the counterparty to every large swap, 0DTE block, and barrier option, their automated hedging requirements dictate the intraday path of least resistance for the price.

Exploiting Negative Gamma Flushes: When market-making desks are in a “Negative Gamma” regime, their algorithms are mechanically forced to sell as the price drops and buy as the price rises, heavily accelerating volatility. If you see an index enter a deep negative gamma zone via market data feeds, stop buying the dip. Instead, buy out-of-the-money puts or short equity index futures to ride the forced algorithmic liquidation cascade.

Trading the Gamma Wall Pin: A massive concentration of positive institutional gamma at a specific strike price acts as a structural ceiling. Market makers will actively sell into rallies approaching this wall. When you identify a major Gamma Wall via open interest data, avoid buying breakout options. Instead, execute options credit spreads or sell premium outside the wall, profiting from the structural containment.

2. Front-Running the Dispersion Trade

When institutional dispersion trades are highly active, the implied volatility of individual stocks becomes heavily overstated relative to the implied volatility of the index. You can spot this by tracking the Cboe Dispersion Index (DSPX).

When the dispersion index reaches historical extremes, it signals that index options are artificially cheap due to institutional selling, while individual stock options are drastically overpriced. As a retail trader, you can exploit this asymmetry in the options market by buying structural straddles or strangles on the index futures/options, betting on a normalization of volatility, or utilizing defined-risk vertical spreads on individual equities to capture the inflated individual option premium.

3. Tracking Barrier Magnetism and Volatility Skew

Hidden barriers in structured notes and custom volatility swaps leave a distinct fingerprint on the Implied Volatility (IV) Skew—the difference in implied volatility between out-of-the-money puts and calls.

If a stock is drifting lower and you notice that the IV of puts at a specific downside strike is exploding at an absolute parabolic rate compared to nearby strikes, you are likely looking at a major institutional barrier level. Rather than fighting the trend, futures traders can look to short contract pullbacks toward that level, as the stock will be structurally dragged toward the barrier by the issuing banks’ forced delta short-hedging.

How to Trade the Structural Reality

Stop trading purely based on traditional retail patterns like head-and-shoulders or simple moving average crossovers. When you enter a position, ask yourself a simple question: Who is currently being forced to buy or sell this asset?

| Sneaky Structure | Market Metric Signal | Institutional Reality | The Tactical Retail Trade |

| 0DTE Gamma Squeeze | Massive intraday call volume surge + Rapidly shifting intraday delta metrics. | Market makers are forced to aggressively buy underlying spot shares to hedge. | Long ATM/Slightly OTM calls or long futures to scalp the highly predictable, algorithmic momentum wave. |

| Dispersion Suppression | Elevated Cboe Dispersion Index (DSPX) + Flat index price action. | Index volatility is mechanically suppressed while underlying names churn violently. | Sell premium on the index via Iron Condors; buy defined-risk premium on volatile individual components. |

| Barrier Option Trap | Parabolic put IV skew acceleration at a specific out-of-the-money downside strike. | Issuing banks are structurally forced to short more stock as the barrier approaches. | Short micro/mini futures or buy puts targeting the exact barrier strike. Benefit from the forced mechanical flush. |

By shifting your focus from vague market sentiment to concrete institutional flow, dealer positioning, and delta exposure data, you effectively strip away Wall Street’s primary advantage. You stop guessing where the price is going, and start positioning yourself precisely where big capital is structurally forced to push it.

Leave a Comment

You must be logged in to post a comment.