Institutional trading algorithms operate in a completely different universe than retail day traders. The modern stock market is no longer a physical floor of shouting brokers; it is a digital battlefield dominated by machines. While a retail trader might look at a chart and wait for a standard indicator like a Moving Average to cross, institutional algorithms are hunting for microscopic, mathematical inefficiencies.

Built by quantitative hedge funds and high-frequency trading (HFT) firms, these algorithms are essentially sets of highly complex, pre-programmed rules. They do not feel fear, greed, or hesitation. When specific market conditions align, the algorithm triggers a trade in a fraction of a millisecond without any human intervention.

For the everyday retail trader, this reality can seem deeply intimidating. How can a human competing on a standard internet connection possibly edge out a billion-dollar machine? The secret is not to out-speed them, but to understand their programming. By knowing exactly what triggers these emotionless and mathematical systems, retail traders might want to think about the opportunity to piggyback on their massive wake.

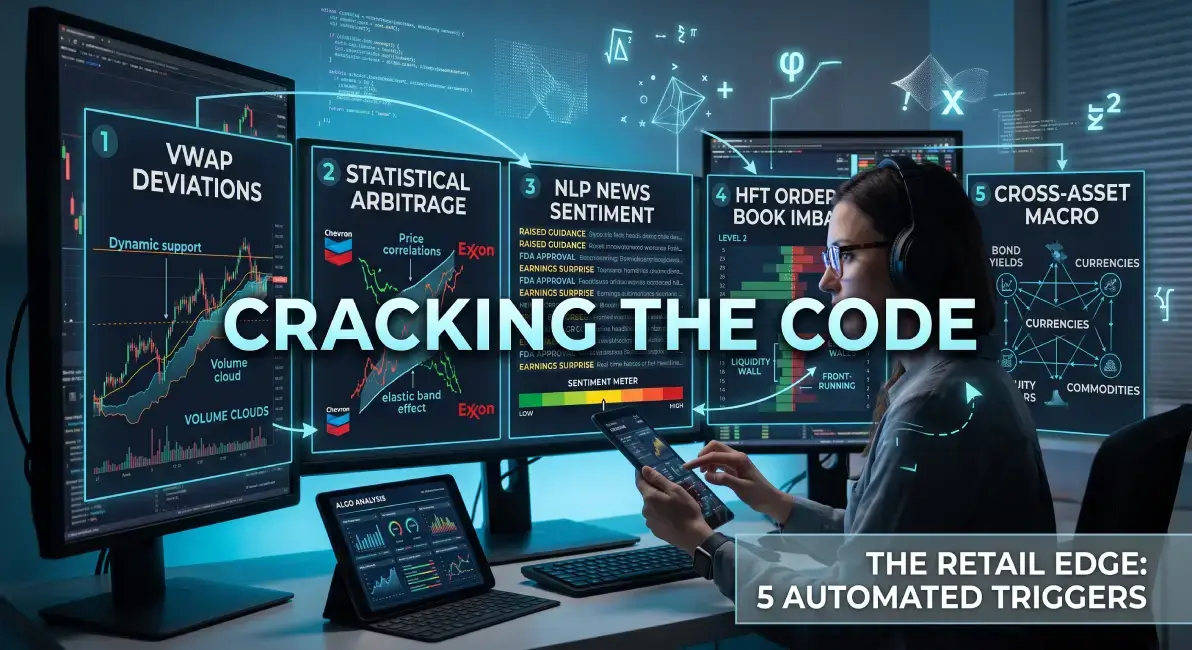

Here are the top five primary automated triggers that drive institutional trading algorithms, along with potential strategies for retail traders to think about in theory.

1. VWAP/TWAP Deviations: Hiding the Giant’s Footprint

When a massive mutual fund wants to buy 5 million shares of Apple, they cannot buy it all at once, or they would cause the stock price to instantly skyrocket, giving them a terrible average price. Instead, they use execution algorithms to hide their footprint.

The Institutional Trigger: These algos are triggered by Volume-Weighted Average Price (VWAP) or Time-Weighted Average Price (TWAP). The algorithm constantly monitors the day’s average price based on trading volume. If the current live price dips slightly below the VWAP, the algorithm automatically triggers a “buy” order for a small chunk of shares, such as 500 shares. It does this thousands of times throughout the day to secure a massive position at the best mathematically possible average price.

The Potential Retail Strategy (The Edge):

As a retail trader, VWAP is one of the most powerful indicators that traders can put on their day-trading chart. Because institutions are mathematically programmed to accumulate shares when the price dips below this average, VWAP often acts as a massive, invisible level of dynamic support. Retail traders might build a strategy around “VWAP pullbacks.” Instead of considering buying breakouts—which often fail—retail traders can think about waiting for a strong stock to dip to the VWAP line. Knowing that execution algorithms are likely waiting there to scoop up blocks of shares, retail traders can think about entering long positions with tight risk management right at the VWAP line, potentially riding the coattails of the mutual fund’s accumulation.

2. Statistical Arbitrage (StatArb): The Elastic Band Effect

Statistical arbitrage algorithms look for historical correlations between two or more assets. These systems rely heavily on mean reversion, assuming that anomalies between closely linked equities will eventually correct themselves.

The Institutional Trigger: The trigger for these algorithms is a microscopic breakdown in a historical pricing relationship. Let’s say ExxonMobil and Chevron stock prices typically move in perfect lockstep. Suddenly, a massive seller dumps Chevron, causing its price to drop by 0.2%, while Exxon stays flat. The StatArb algorithm is triggered instantly by this mathematical divergence. It automatically buys Chevron (the relatively cheap asset) and short-sells Exxon (the relatively expensive asset), knowing that the historical correlation will eventually snap back into place.

The Potential Retail Strategy (The Edge):

Retail traders might be able to think about capitalizing on statistical arbitrage by utilizing “Pairs Trading.” By identifying two highly correlated assets—such as Visa and Mastercard, or Coca-Cola and Pepsi—traders could potentially map their price ratio on a charting platform. When breaking news or sudden, unexplained volume causes one stock to drop while the other remains flat, it’s possible that StatArb algorithms will step in to correct the inefficiency. Retail traders can potentially mimic this by thinking about buying the undervalued stock and selling the overvalued one (or just focusing on the undervalued one), considering the potential snap-back. The potential edge here is patience; wait for the elastic band to stretch to an extreme before contemplating entering the trade.

3. Natural Language Processing (NLP) / News Sentiment: The Millisecond Readers

In the modern era, reacting to the news is no longer a human endeavor. Many quantitative funds plug their algorithms directly into machine-readable news feeds from Bloomberg, Reuters, or even social media APIs.

The Institutional Trigger: These systems look for specific keywords, sentiment scores, or SEC Edgar filings. If a company releases an earnings report, an NLP algorithm scans the entire document in microseconds. If it detects phrases like “raised guidance,” “record margins,” or “FDA approval,” the algorithm calculates a positive sentiment score and triggers a massive buy order. This happens before a human analyst has even finished reading the headline.

The Retail Strategy (The Edge):

It might not be a good idea to try to race a machine on breaking news. Traders might always lose. The potential retail edge lies in trading the “second wave” or the “overreaction fade.” Because NLP algorithms buy aggressively based on keyword triggers, they can often create extreme, unnatural price spikes. If an algorithm sees “FDA approval” and bids a stock up 15% in two seconds, human traders might eventually step in to evaluate the actual financial impact. If the news isn’t as good as the raw keyword suggests, the stock might crater. Retail traders might think about capitalizing by waiting for the initial 5-minute algorithmic dust to settle. If the stock establishes a base and holds its gains, traders might want to think about trading the human-driven momentum continuation. If it immediately stalls, traders might want to think about a short on the algorithmic overreaction as prices potentially revert to reality.

4. Market Microstructure & Order Book Imbalances: The HFT Plumbing

High-Frequency Trading firms don’t care about the actual companies; they care about the “plumbing” of the stock market. Their battlefield is entirely within the data that most casual traders ignore.

The Institutional Trigger: HFTs look at the Level 2 Order Book, which is the queue of all pending buy and sell limit orders. They are triggered by bid-ask spread anomalies or sudden “weight” shifts in the order book. If an HFT algorithm detects a massive wall of buy orders queuing up at a specific price, it will trigger a “front-running” trade. It buys the stock milliseconds before the massive institutional order executes, and then instantly sells it back to the institution a fraction of a cent higher. They do this millions of times a day to scalp fractions of pennies.

The Retail Strategy (The Edge):

Retail traders probably cannot compete in scalping fractions of a penny. However, by learning to read the Level 2 Order Book, traders might be able use the HFT’s behavior to their advantage. HFTs react to “liquidity walls” (large stacks of limit orders). Retail traders might want to think about using these walls as high-probability support and resistance zones. If there’s a massive institutional buy order queued at $50.00, it’s possible HFTs might be aggressively buying at $50.01 to front-run it. Instead of guessing where a stock will bounce, traders might want to think about positioning their own limit orders just above these institutional walls, potentially allowing the heavy algorithmic volume to act as a safety net for potential trades.

5. Cross-Asset Macro Triggers: The Interconnected Web

Financial markets are deeply interconnected. Equities, bonds, currencies, and commodities all impact each other, and institutional algorithms are well aware of this web.

The Institutional Trigger: The trigger is a sudden movement in a correlated external market. For example, an algorithm trading the S&P 500 (SPY) might be hardwired to watch the 10-Year Treasury Yield. If bond yields suddenly spike upward by 3 basis points in one second, the algorithm is mathematically programmed to recognize that higher yields hurt tech stocks. The algorithm will automatically trigger sell orders on the Nasdaq 100 before the equity market has even fully registered the bond movement.

The Retail Strategy (The Edge):

The vast majority of retail stock traders only look at the stock they are trading. To potentially gain an institutional edge, traders might want to consider building a macro-dashboard. If traders are day-trading tech stocks (like the QQQ), they could think about having a live chart of the 10-Year Treasury Yield and the US Dollar Index (DXY) on their screen. By potentially watching these correlated external markets, traders might be able to anticipate algorithmic equity flows. If the US Dollar suddenly plummets, its plausible that algorithms could trigger buy programs for large-cap multinational stocks. Trading with a macro perspective might allows traders to think about acting proactively rather than reactively.

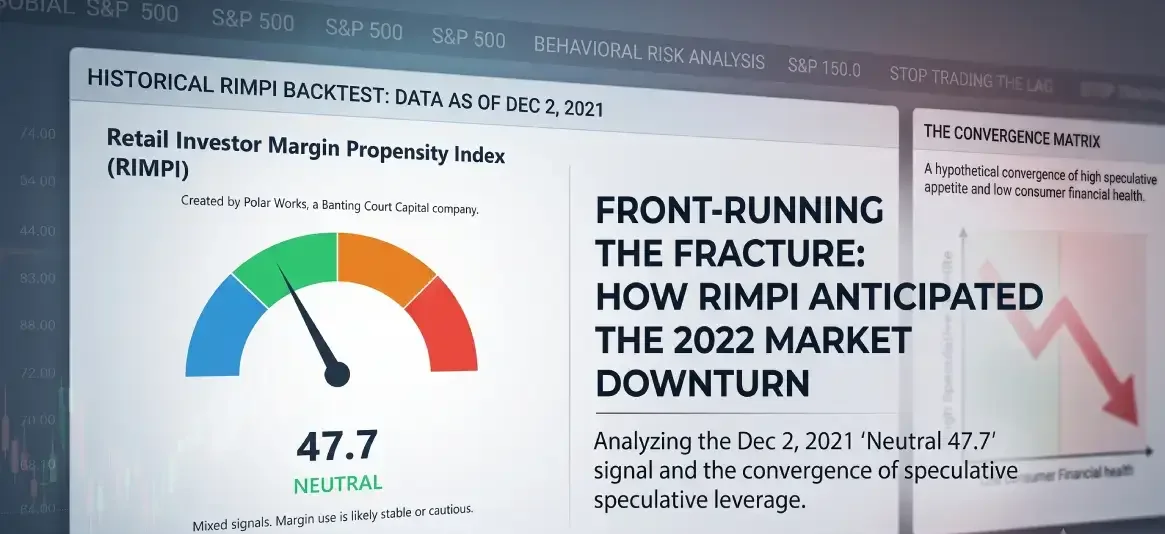

More to Think About

The stock market is undoubtedly ruled by machines that execute trades faster than the human brain can process. However, to help visualize how emotionless and mathematical these systems are, traders only have to look at the strict rules they follow. They do not possess intuition, and they cannot deviate from their programming.

By understanding the five primary automated triggers of institutional trading algorithms—VWAP deviations, statistical arbitrage, news sentiment, order book imbalances, and macro correlations—retail traders might be able to stop fighting the tape. Instead of being the prey in a machine-dominated market, traders could potentially learn to map the predators’ footprints and build highly profitable, strategic edges alongside them.

Leave a Comment

You must be logged in to post a comment.