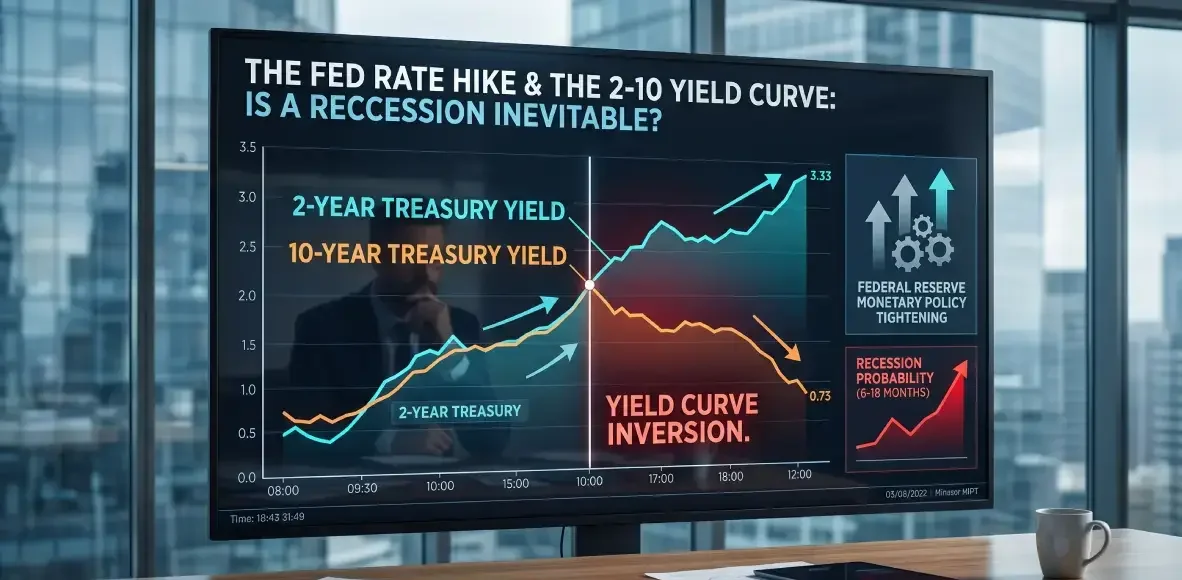

In the complex world of macroeconomic forecasting, few indicators command as much respect—and incite as much anxiety—as the 2-10 yield curve. This financial metric, representing the spread between the 10-year and 2-year U.S. Treasury yields, is widely regarded as a severe warning sign for the economy when trending downward. When the curve is upward-sloping, it signals healthy economic expansion. But when it flattens and eventually inverts, warning sirens begin to blare across Wall Street.

The stakes are remarkably high. Historical data paints a sobering picture: an inverted yield curve has led to a recession 6 to 18 months later nearly every time in the last 55 years. Today, as the Federal Reserve contemplates another rate hike to cool the economy, the yield curve is dangerously close to this critical inversion point. Will a prospective 25-basis-point hike push the economy over the edge? Or can central bankers engineer a legendary “soft landing”?

The Current State of the 2-10 Yield Curve

To understand the gravity of the impending Federal Reserve decision, we must first examine the current structural mechanics of the bond market. Over the last six months, the yield curve has exhibited a definitively hostile trend, aggressively flattening by 40 basis points as it dropped from a healthy 0.68% down to a precarious 0.28% (28 basis points). This rapid compression definitively proves that bond investors are growing increasingly pessimistic about long-term economic growth.

Presently, the margin for error is effectively zero. The 10-2 spread is sitting at just 28 basis points, which is practically identical to the size of a proposed 25-basis-point Fed rate hike. The bond market operates strictly on what is “priced in” by investors. Right now, futures markets are assigning a 51.7% probability to a September rate hike. Because this is essentially a coin flip, the 2-year Treasury yield is currently only reflecting about half of the reality of that impending 25-basis-point hike.

The Mathematical Constraints of a Rate Hike

If the Federal Reserve moves forward with a 25-basis-point rate hike in September under these exact conditions, an inversion of the 2-10 yield curve becomes highly probable, both leading up to the decision and immediately after. As economic data solidifies the likelihood of a hike, pushing that 51.7% probability toward 100%, the 2-year yield will organically rise by roughly 12 to 15 basis points to fully absorb the reality of the impending hike.

Specifically, the short end of the curve must absorb the remaining unpriced ~48.3% of the 25 bps hike. This translates to an upward move of roughly 12 basis points on the short end. If we subtract that 12-basis-point adjustment from the current 28-basis-point spread, the new baseline becomes 16 basis points. This mathematical adjustment alone compresses the curve down to roughly 13 to 15 basis points before the Fed even meets in September.

Before the market even has time to digest the broader economic implications, the sheer mechanical adjustment of the 2-year yield compressing to the new Fed Funds rate leaves you with a microscopic 16-basis-point buffer from inversion. For the curve to successfully avoid inversion, that 16-basis-point buffer must hold. This means the 10-year yield must either stay perfectly flat or rise. Unfortunately, market behavior suggests the exact opposite is about to occur.

The “Policy Error” and the Bear Flattener

When the Federal Reserve executes a rate hike while the yield curve is already flattening aggressively, it triggers a dynamic bond traders call a bear flattener. In this scenario, short-term rates are forced up because they must match the Fed’s new, higher policy rate. Conversely, the long end of the curve (the 10-year yield) is dictated by the market’s long-term outlook on growth and inflation.

If the bond market believes the Fed is hiking rates too late in an economic cycle, it interprets the move as restrictive policy that will eventually choke off economic growth. In response to growth fears, institutional investors buy 10-year Treasuries as a safe haven to lock in yields before the economy stalls. Buying pressure drives bond prices up, which inherently drives yields down.

Consequently, as the 2-year yield is forced upward by the Fed and the 10-year yield gets pulled downward by investors seeking safety, that remaining gap evaporates instantly, locking in the inversion. Because the proposed hike (25 basis points) is practically identical to the remaining spread (28 basis points), the margin for error is effectively zero. Given that the remaining buffer is only ~16 bps, the structural momentum of the market practically guarantees that the 10-year yield will sink fast enough to wipe out that gap, dropping the spread below 0.00. Therefore, the odds of inversion in this specific scenario are exceptionally high—likely exceeding 80% to 90%.

Is Inversion (and Recession) Inevitable?

With an 80-90% probability of inversion looming, and the ominous 55-year track record of recessions following inversions (6-18 months later), panic seems like a rational response. However, is it inevitable? The short answer is no.

The yield curve is not bound by laws of physics. It is a reflection of bond market expectations versus Federal Reserve policy. A 10-2 yield curve dropping below 0.30% is a critical diagnostic tool indicating that the economic cycle is running out of runway. It signals that monetary policy is too tight and is choking off economic growth. However, it is not a point of no return. Historical data proves it can reverse course without crossing the 0.00% inversion threshold.

When the curve approaches zero but abruptly steepens back upward, it is often the result of a “mid-cycle adjustment” or a “soft landing”. If the Federal Reserve recognizes this and reacts proactively—usually by pausing rate hikes or executing “insurance” rate cuts—the yield on the highly sensitive 2-year Treasury plummets faster than the 10-year yield. This pivots the curve back into a normal, upward-sloping trajectory before an inversion can actually lock in.

Historical Soft Landings: When the Fed Got It Right

History provides several textbook examples of the most famous “near misses,” where the curve dropped below 0.30% after a long downtrend but successfully avoided a persistent inversion and a subsequent recession.

The 1994-1995 Soft Landing: This is the textbook example of the curve reaching the brink and bouncing back. In early 1994, the 10-2 spread was a healthy 1.50%. Worried about inflation, Fed Chair Alan Greenspan aggressively doubled the federal funds rate from 3% to 6% over a 12-month period. As short-term rates rocketed upward, the curve flattened continuously. By December 1994 and into early 1995, the 10-2 spread compressed all the way down to roughly 0.10% (10 basis points). Instead of pushing the economy into a recession, the Fed paused its rate hikes and initiated a slight rate cut in mid-1995. The curve never inverted, the economy stabilized, and the U.S. entered one of the greatest bull markets in history.

The 1998 Global Contagion Pause: This period featured the flattest non-inverted yield curve in modern history. Following the Asian Financial Crisis and heading into the collapse of the Long-Term Capital Management (LTCM) hedge fund and the Russian debt default, global investors flooded into long-term U.S. Treasuries as a safe haven. This drove the 10-year yield down rapidly, flattening the curve for well over a year. By May and June of 1998, the 10-2 spread dropped well below 30 basis points, eventually touching exactly 0.00% (and briefly ticking negative by 1 or 2 basis points intraday before closing flat). Facing a frozen credit market, the Fed executed a series of rapid emergency rate cuts in the fall of 1998. The 2-year yield collapsed in response, the curve steepened violently back into positive territory, and the economic expansion survived until the dot-com bust in 2001.

The 1984 Mid-Cycle Adjustment: Following the brutal double-dip recessions of the early 1980s, the economy was booming, but inflation fears lingered. Fed Chair Paul Volcker initiated a sharp tightening cycle in 1983 and 1984, raising the federal funds rate from roughly 8.5% to over 11.5%. The 10-2 spread, which had been over 1.50%, trended downward for months until it bottomed out between 0.15% and 0.20% (15 to 20 basis points) in the late summer of 1984. Inflation remained under control, and the Fed began easing rates late in the year. The yield curve steepened, avoiding inversion, and the 1980s economic expansion continued unimpeded.

Insights for Investors

Navigating a potential 2-10 yield curve inversion requires a strategic approach rather than emotional reactions. Based on the structural mechanics of the bond market and historical precedents, here are actionable steps investors should consider:

Monitor the Fed’s Rhetoric closely: A 10-2 yield curve dropping below 0.30% is a critical diagnostic tool. If the Fed signals a pause or hints at insurance cuts in response to slowing growth, the likelihood of a mid-cycle adjustment increases, creating a bullish environment for equities.

Prepare for the Bear Flattener: If the Fed pushes through with a hike despite a shrinking buffer, expect safe-haven assets to rally. High-quality long-term Treasury bonds generally appreciate in price as institutional investors flock to safety and inherently drive yields down.

Assess Defensive Sectors: Because an inverted curve has preceded recessions consistently over the last 55 years, a confirmed inversion should prompt a portfolio review. Market participants might consider rotating a portion of equity exposure into recession-resistant sectors.

Don’t Panic Sell: An inversion is a leading indicator, often preceding a recession by 6 to 18 months. Markets can still experience significant gains in the period immediately following an inversion before a downturn materializes.

Coming Full Circle

The prospect of a Federal Reserve rate hike into a rapidly flattening yield curve presents a precarious mathematical and behavioral challenge. When the Fed hikes into a flat curve, an inversion is the path of least resistance. With the current spread offering virtually no margin for error, an 80-90% probability of inversion stands if the Fed proceeds aggressively. While the ominous 55-year recession indicator cannot be ignored, history reminds us that it is not a point of no return. As 1984, 1995, and 1998 prove, if central bankers adjust liquidity quickly enough in response to that 30-basis-point warning light, the curve can organically steepen without an inversion or a recession taking place. So will the Fed raise rates? Or will it opt for a cut?

Leave a Comment

You must be logged in to post a comment.